Wall Street closes at a record for the first time since end of January

ASA International Group plc (LON:ASAI) presented its fiscal year 2025 results on April 15, 2026, revealing a dramatic profitability surge as the microfinance lender’s operational leverage delivered nearly double the net profit while expanding across emerging markets. The company’s stock responded positively, climbing 7.01% to 214 pence, extending a remarkable 168.5% gain over the past year.

Executive Summary

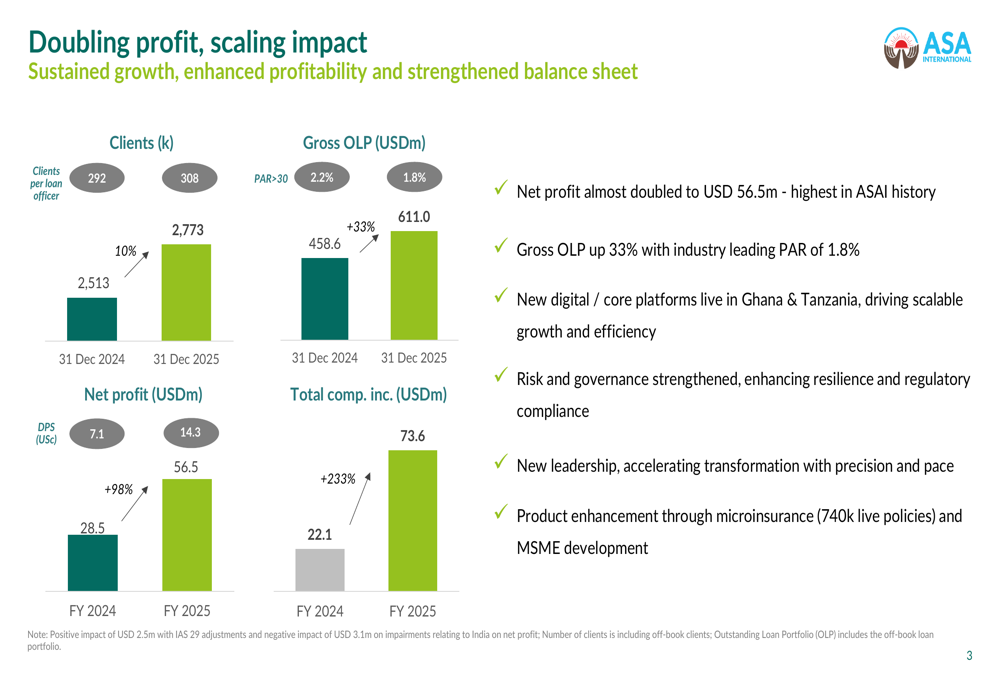

The London-listed microfinance institution reported net profit of $56.5 million for FY 2025, representing a 98% increase from $28.5 million in the prior year. This marked the highest profitability in the company’s history, driven by a 33% expansion in gross outstanding loan portfolio (OLP) to $611.0 million and significant improvements in operational efficiency.

As demonstrated in the company’s results overview, ASA International achieved growth across multiple key performance indicators while maintaining industry-leading asset quality.

Total comprehensive income surged 233% to $73.6 million, while return on average equity improved from 33.0% to 43.8%. The company also doubled its dividend per share to 14.3 US cents from 7.1 cents, reflecting confidence in sustainable profitability.

Operational Leverage Drives Profitability

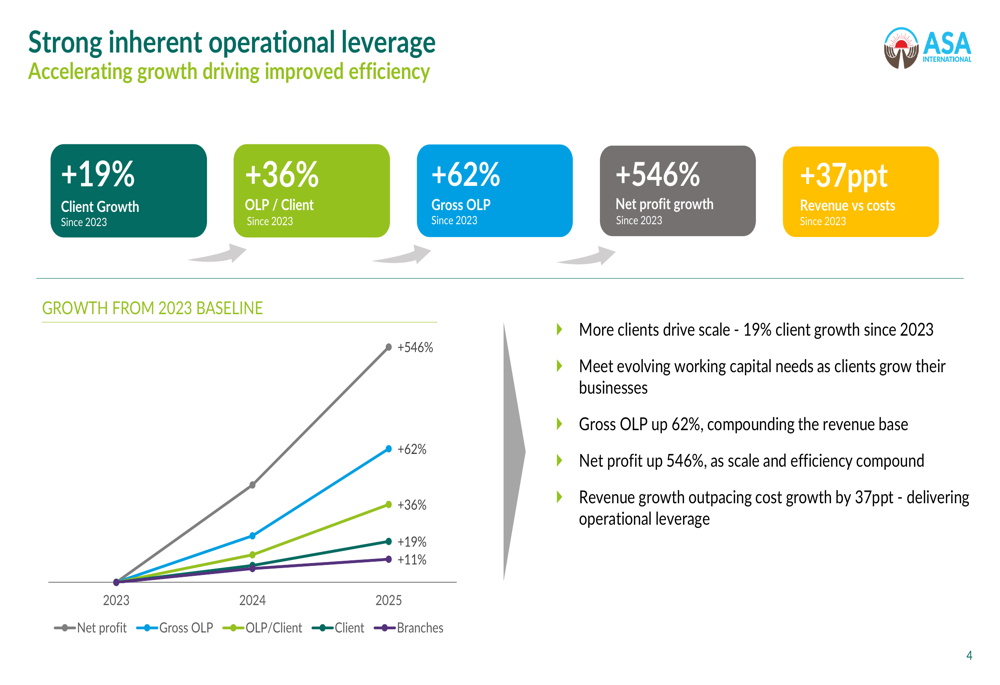

The presentation emphasized ASA International’s ability to convert growth into accelerating profits through operational leverage. Since 2023, the company has grown its client base by 19% to 308,000 while increasing loan portfolio per client by 36%, compounding revenue growth.

The following chart illustrates how revenue growth has dramatically outpaced cost increases, with net profit growing 546% since the 2023 baseline.

Revenue growth outpaced cost growth by 37 percentage points since 2023, demonstrating the scalability of ASA’s microfinance model. The cost-income ratio improved to 56.8% from 61.4%, as operating income rose 39% to $260.1 million while total operating expenses increased just 29% to $143.4 million.

Net Interest Margin Expansion

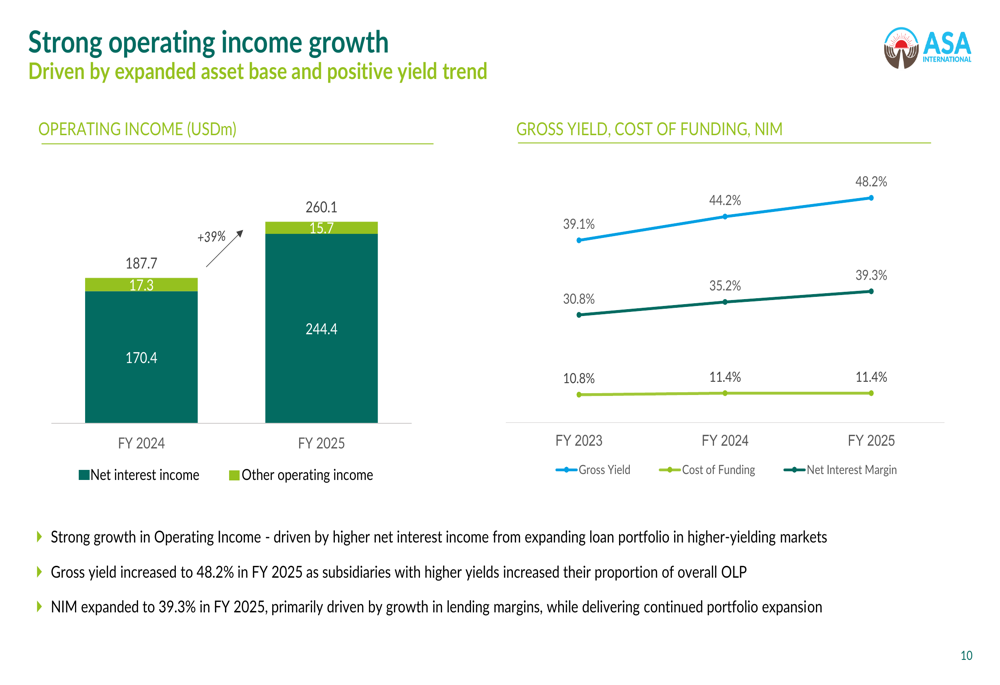

ASA International achieved substantial margin expansion during the year, with net interest margin (NIM) reaching 39.3%, up from 35.2% in FY 2024. Gross yield on the loan portfolio increased to 48.2% while cost of funding remained stable at 11.4%.

The company’s operating income growth was driven primarily by net interest income expansion, as shown in the following breakdown.

Net interest income grew 43% to $244.4 million, fueled by the expanding loan portfolio and improved pricing. This more than offset a modest 9% decline in other operating income to $15.7 million.

Regional Performance Analysis

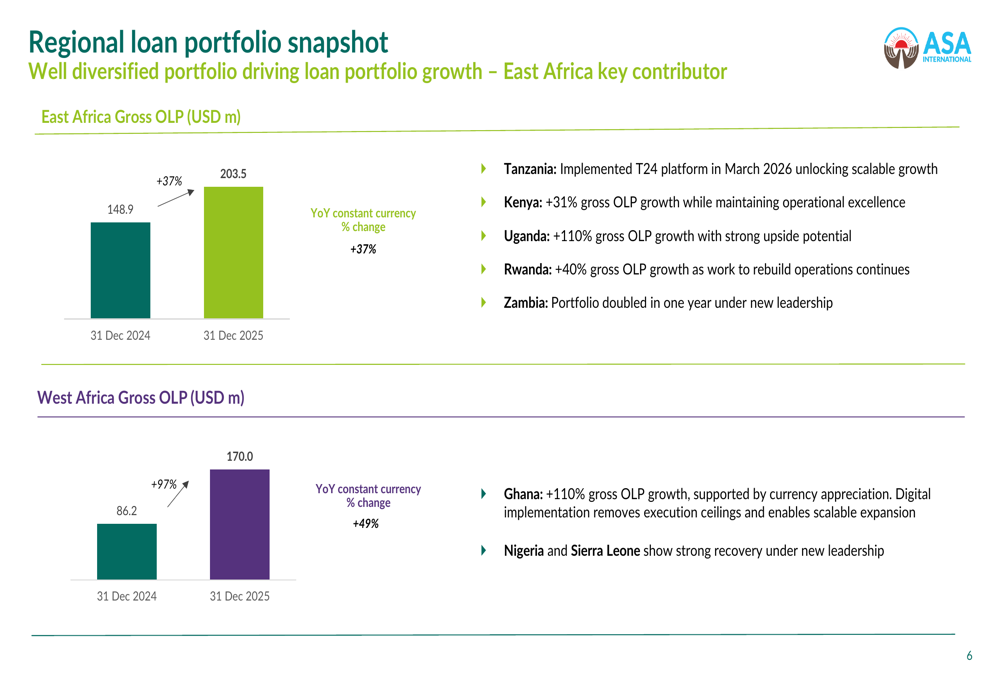

ASA International demonstrated strong geographic diversification with particularly robust growth in West Africa. The region’s gross OLP surged 97% in reported terms to $170.0 million, or 49% growth in constant currency terms.

Ghana led the West African expansion with 110% OLP growth, supported by local currency appreciation. Nigeria and Sierra Leone showed "strong recovery under new leadership," according to the presentation.

East Africa delivered more moderate but steady 37% OLP growth to $203.5 million, with particularly strong performances in Uganda (+110%) and Zambia (portfolio doubled). Kenya maintained 31% growth "while maintaining operational excellence."

In South Asia excluding India, the portfolio grew 31% to $124.7 million, driven by Pakistan’s rapid scaling under new leadership. However, the company continued its deliberate wind-down in India, where OLP declined 25% to $30.2 million. South East Asia saw a 6% reported decline to $82.5 million, though this represented 12% growth in constant currency terms.

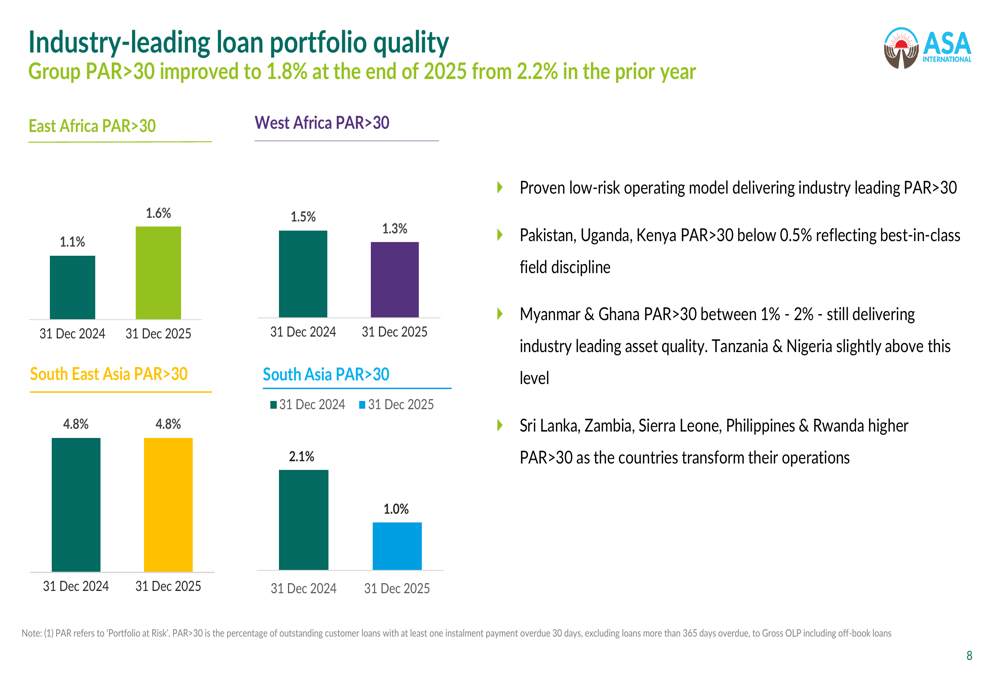

Industry-Leading Asset Quality

Despite rapid portfolio expansion, ASA International maintained exceptional credit quality with portfolio at risk over 30 days (PAR>30) improving to 1.8% from 2.2% in the prior year.

The company’s proven low-risk operating model delivered strong asset quality across most regions, as illustrated in the following portfolio quality metrics.

Pakistan, Uganda, and Kenya each achieved PAR>30 below 0.5%, while Myanmar and Ghana maintained levels between 1-2%. The presentation noted that Sri Lanka, Zambia, Sierra Leone, Philippines, and Rwanda experienced higher delinquency rates but remain under management focus.

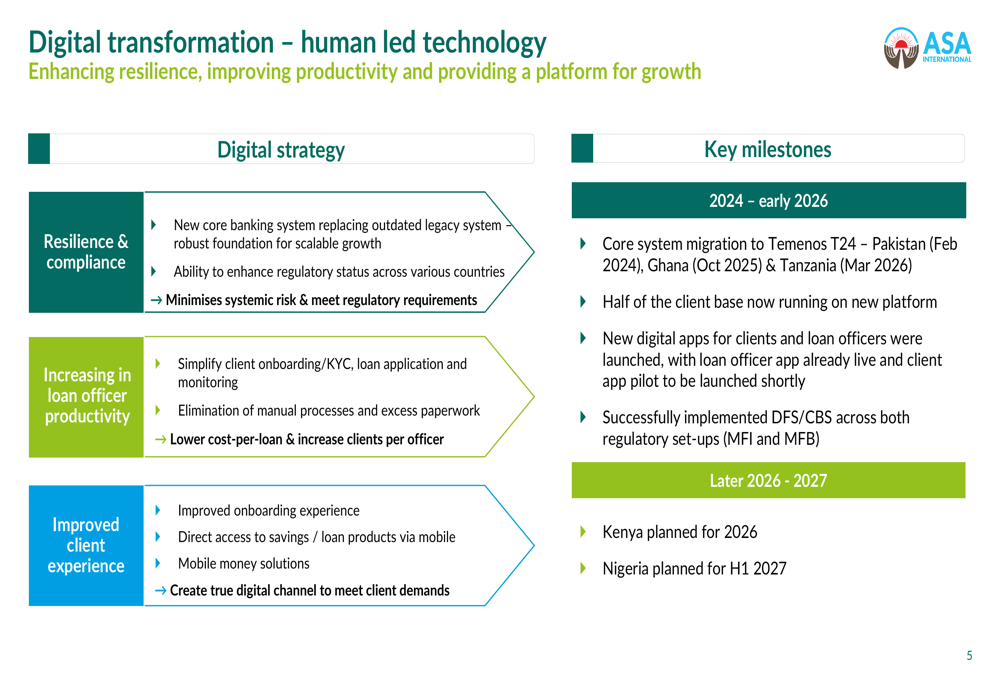

Digital Transformation Progress

A key strategic initiative highlighted in the presentation was ASA’s "human-led technology" digital transformation, centered on migrating to the Temenos T24 core banking platform and launching digital financial services.

By March 2026, the company had successfully migrated Pakistan (February 2024), Ghana (October 2025), and Tanzania (March 2026) to the new platform, representing half of the client base. Kenya is planned for 2026 with Nigeria following in H1 2027.

The digital strategy aims to increase loan officer productivity through simplified onboarding and KYC processes, improve client experience with mobile access to savings and loan products, and enhance regulatory compliance while minimizing systemic risk.

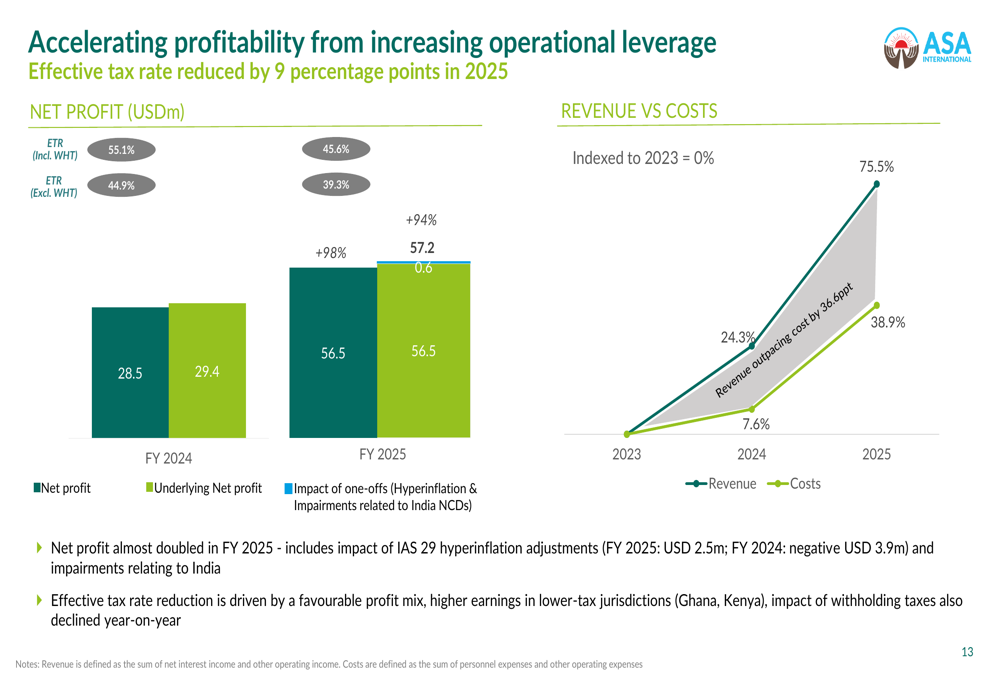

Profitability Acceleration

The company’s net profit growth significantly outpaced revenue expansion, demonstrating the operating leverage embedded in the business model.

Underlying net profit reached $56.5 million before one-time items, while the effective tax rate improved from 55.1% to 45.6% including withholding taxes, or from 44.9% to 39.3% excluding WHT. Management attributed the tax rate reduction to improved profit mix across jurisdictions.

The presentation showed revenue indexed growth of approximately 80% since 2023, while costs grew roughly 43%, creating a 36.6 percentage point gap that flowed through to profitability.

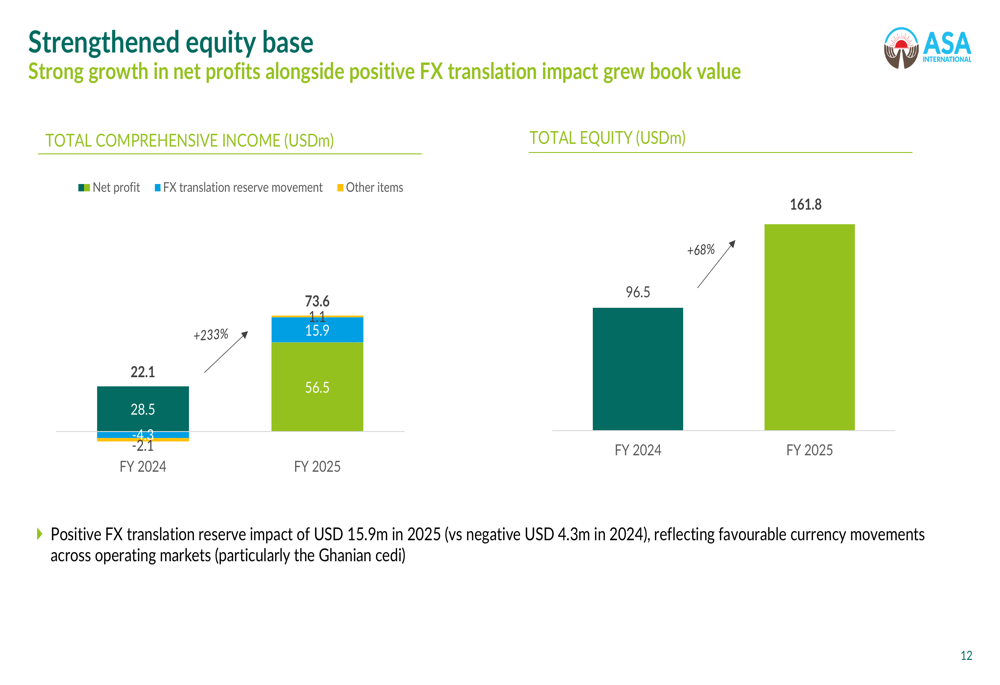

Strengthened Capital Position

ASA International’s equity base expanded 68% to $161.8 million, supported by strong earnings retention and positive foreign exchange translation effects of $15.9 million.

The funding mix evolved with local deposits increasing to $136.7 million from $90.1 million, in line with the company’s strategy to diversify funding sources. Total interest-bearing debt grew 32% to $412.4 million, maintaining a favorable maturity profile with $150.8 million due within three months and $243.7 million in the 1-5 year bucket.

The company maintained minimal foreign exchange risk with 99.8% of loans either hedged or in local currency.

Strategic Priorities and Product Expansion

Beyond core microfinance lending, ASA International highlighted several strategic initiatives for sustainable growth. The company launched a microinsurance product that achieved 740,000 life policies in force, and developed a Micro SME proposition to serve evolving client needs.

The presentation outlined six top strategic priorities: enhancing the client journey, completing digital transformation, achieving operational excellence, growing deposits, optimizing capital allocation, and selective new country expansion.

Management emphasized that 286,000 community members benefited from various social programs during the year, and the company joined the Client Protection Pathway while continuing environmental initiatives including solar panel installations.

Market Context and Outlook

Trading at 214 pence following the 7.01% post-announcement surge, ASA International shares have delivered exceptional returns but also exhibit high volatility with a beta of 2.0. The stock has traded in a 52-week range of 82.5 to 248 pence.

The company’s outlook statement noted continued monitoring of the Middle East situation while emphasizing that "fundamentals of the business remain strong" with resilient client demand for loans expected. Management highlighted ongoing focus on productivity improvements as digital platforms scale.

With a recommended final dividend bringing the full-year payout to 14.3 US cents per share—double the prior year—ASA International demonstrated confidence in sustaining its profitability trajectory while continuing to invest in digital infrastructure and geographic expansion across its emerging market footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.